This article guides small business owners through practical bookkeeping strategies to ensure accurate records, maintain compliance, and make informed financial decisions. From setting up accounts and choosing the right accounting method to understanding tax obligations and adopting best practices, you’ll learn how to keep your business financially healthy and future-ready.

What you’ll learn:

- Why a separate business bank account is essential

- How to structure your chart of accounts effectively

- The difference between accrual and cash accounting

- Which financial management systems suit small businesses

- Key recordkeeping rules from the Australian Tax Office (ATO)

- GST registration thresholds and compliance requirements

As a business owner, you face many obstacles. And bookkeeping for small businesses can be one of your greatest challenges, especially when trying to tackle the books all by yourself.

For one, there’s the considerable time it takes each month to enter data and the potential for errors and miscalculations. Not to mention the possible consequences of using incorrect financial reports in business decision-making if you do get something wrong.

Without proper bookkeeping, small businesses in Australia could miss out on tax deductions they are entitled to or even experience cash flow problems that could put financial viability at serious risk.

Typically, business owners are experts in their area of business, but very few are bookkeeping, GST and tax compliance experts as well.

In our latest blog, we explore how you, as a small business owner, can effectively manage your books to ensure your financial records are accurate, you maintain compliance and steer clear of any problems with the Australian Tax Office (ATO).

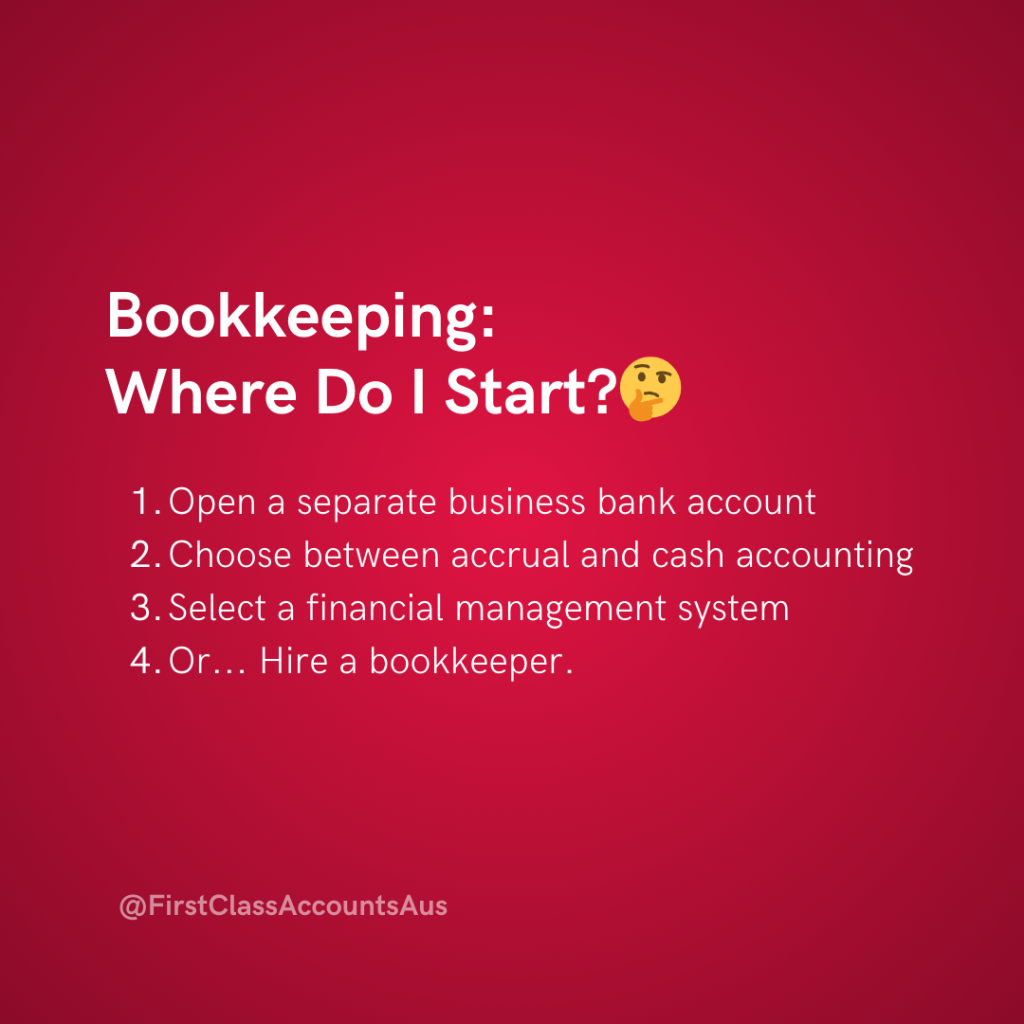

Bookkeeping for Small Business in Australia –

Where Do I Start?

First thing’s first.

Ensure you have a separate account specifically for your business

It might go without saying, but to effectively manage your business finances, you absolutely should have a separate bank account for your business. For some business structures, it is a legal requirement to do so (partnerships, companies, and trusts must have a separate account for tax purposes). But, no matter what your business structure is, having a separate bank account for your business is best practice.

Carefully consider your chart of accounts

A chart of accounts is your framework for managing your business transactions. It is a list of categories that helps you track your cash flow (what money is coming in and what your expenses are) so you can effectively manage money in your business.

What your chart of accounts looks like will depend on the size and focus of your business. It may include categories such as:

- Accounts receivable

- Cash

- Accounts Payable

- Loans Liabilities/Payable

- Wages/salaries

- Utilities

- Advertising

- Insurances

- Capital Equipment

- Office Administration

- Subscriptions

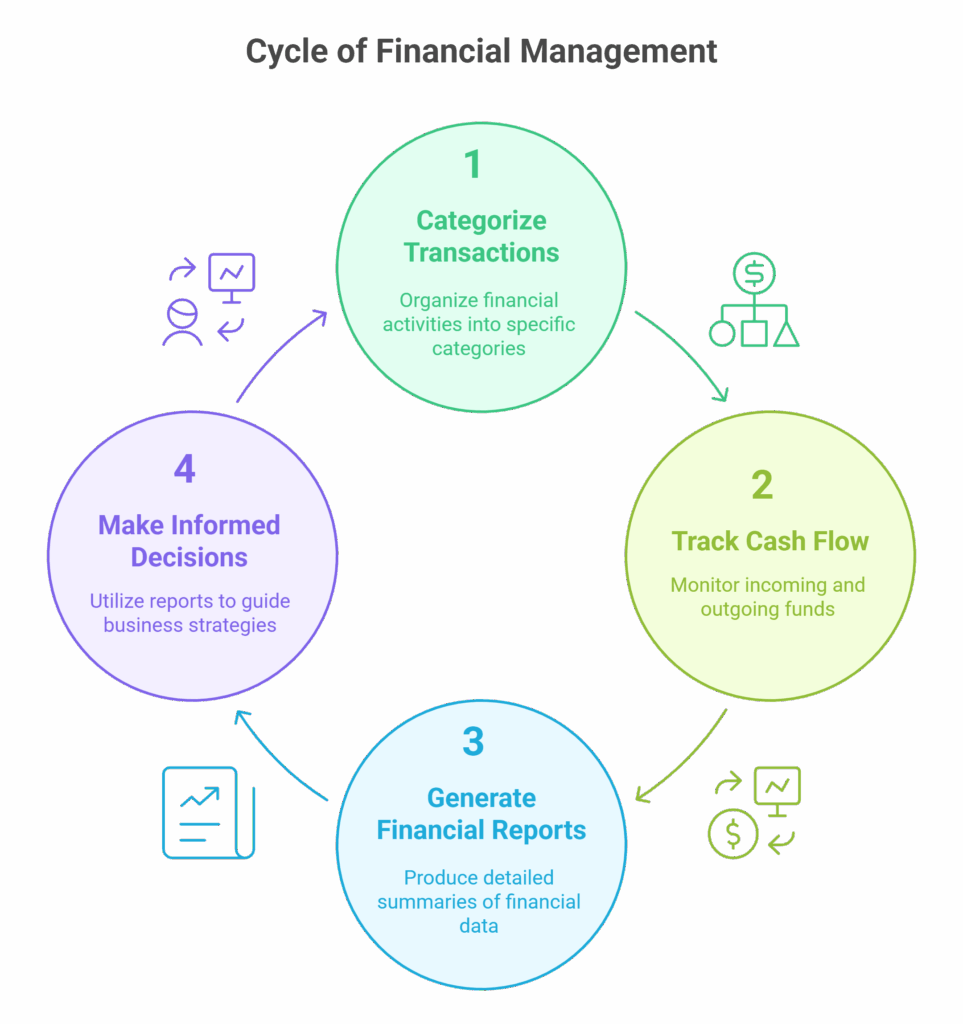

Why is your chart of accounts so important? Because you need to be able to use your financial reports to make informed decisions about your business.

Accrual accounting vs cash

As a small business owner, you need to decide if you will use accrual accounting or cash accounting. Accrual accounting means you record income and expenditure when a transaction happens (for example, when you invoice a customer or when you receive an invoice) and not when the actual money is received or paid.

In contrast, with cash accounting, you would record the income or expenditure when you receive or pay the money, not the invoice date.

Cash accounting may suit smaller-scale businesses. However, accrual accounting shows you the bigger picture and accounts for what you are owed (accounts receivable) and what bills you need to pay (accounts payable).

Decide on what financial management system you will use

There are three main ways a small business can manage its finances:

- A paper-based system (for example, writing transactions in a notebook).

If you have a very small business and trust yourself to keep track of paper-based financial records, this may work for you. However, paper-based financial management systems are not widely used in modern-day business.

- Spreadsheets

If you have very few transactions in your small business, a spreadsheet is one way you can keep track of your income and expenses. Spreadsheets are limited in their capabilities and it can be difficult to spot errors in data entry, formulas and calculations. Spreadsheets also have very limited reporting capabilities.

- Financial accounting software (recommended for small businesses)

Financial accounting software, such as Xero, MYOB and QuickBooks, is designed to make bookkeeping for small businesses easier. They offer a higher level of security, sophisticated reporting, digital receipt-capturing capabilities, branded invoices, and real-time data you can access to track your financial position. These features do, however, come at a cost. Most software options offer an annual subscription cost or a monthly payment option.

What you choose for your small business will largely depend on the size of your business, your revenue, and the number of transactions you need to process each month.

Already overwhelmed by this exhaustive list? Find a local bookkeeper nearest you.

A Note on Recordkeeping

The ATO states that, in general, businesses must keep records for five years. There are some instances where small businesses will need to keep records for longer. It’s best to check with the ATO directly to obtain the correct recordkeeping requirements and timeframes for your specific business.

Be aware of your tax obligations

The ATO has strict requirements when it comes to registering for GST.

Understand when you need to register for GST

The ATO has strict requirements when it comes to registering for GST. You must register for GST when your business turnover reaches $75,000 or more. This is called the ‘GST Threshold’. You must also register if you are a taxi or limousine travel business regardless of your revenue, and if you plan to claim fuel tax credits for your business.

When you’re registered for GST, you need to be able to correctly record all the GST you receive and all the GST you pay to ensure you can submit an accurate GST return every quarter. Being able to prepare accurate financial statements so you have a good picture of your total revenue and expenses is also critical. Financial management software can help with these reports. Getting professional advice when setting up your bookkeeping systems can also be helpful.

Other regulations

It is important for small business owners to keep updated with all tax and compliance obligations for their business. This includes:

- Pay As You Go (PAYG) tax (if applicable)

- Annual tax lodgements and key dates

- Payroll compliance

- Super payments for staff and associated deadlines

Why is compliance so important?

If you’re a small business owner and you don’t comply with the ATO’s tax and compliance obligations, you could face serious penalties and legal consequences. This includes fines, criminal convictions, and even prison sentences. Imagine also the potential damage to your business image and reputation that your non-compliance could cause.

6 Tips and Tricks to Maintain Best Practice in Bookkeeping for Your Small Business

Here are some tips to start today.

1. Ditch the paper records for digital bookkeeping software

The capabilities of digital bookkeeping software far outweigh what you can achieve with spreadsheets and manual hard-copy systems. You can capture receipts and invoices electronically and run reports to keep track of your business finances.

2. Consider cyber security

Ensure you have cyber security measures in place. Change your passwords often and use two-factor authentication to protect your business’s client and financial data. Make sure you have a secure backup in case something goes wrong.

3. Be consistent

When allocating expenses to your chart of accounts, consistency is key. For example, if you add your business phone as a ‘utilities’ expense one month, continue to do that each month. Don’t put it in ‘utilities’ one month and ‘office expenses’ the next.

4. Keep on top of it

Try to set aside time weekly to add invoices and expenses and keep on top of your business finances. Or, even better, add them as they happen. With receipt-capturing software, it’s easy to add receipts as soon as you buy something for your business.

As a busy business owner, it can be difficult for you to keep track of your finances if you are only updating your books quarterly for your GST return or – even worse – when you’re doing your annual tax return! While a shoebox full of receipts may seem tempting so you don’t have to deal with your finances very often, there are so many benefits of regular bookkeeping.

5. Review financial reports regularly

Small business owners need accurate financial reports to make informed decisions about their businesses. We recommend running Balance Sheet and Profit and Loss reports at least monthly so you can continuously track your financial position.

6. Consider getting professional help

There are many things to consider when outsourcing in your small business. Small business owners tend to outsource tasks they:

- Don’t want to do; or

- Don’t have time to do; or

- Can’t do well themselves and want to ensure they comply with all required laws and regulations.

Does this sound like you?

Contact the friendly team at First Class Accounts if you would like to find out more.

Investment in good bookkeeping practices is an investment in the future of your business

If keeping track of transactions and finances is causing you headaches and you don’t want to do it all alone, reach out to the team at First Class Accounts. We are a trusted and reliable partner for small business owners. We offer bookkeeping services, as well as tax and payroll advice. Whether you need a bookkeeper in Sydney, Melbourne, Brisbane, or someplace else across the country, we can help take the stress out of managing the books for your business. First Class Accounts has more than 120 bookkeepers across five Australian states (VIC, NSW, SA, WA, and QLD), so your nearest bookkeeper is just a few clicks away.

Find a First Class Accounts Bookkeeper near me.

Frequently Asked Questions About Bookkeeping for Small Businesses in Australia

BAS & Tax Compliance for Businesses Business Growth & Strategy