This article provides a practical guide for Australian small business owners to prepare for the 2023/24 End of Financial Year, covering essential ATO compliance requirements, deduction opportunities, and strategies to stay organised and avoid costly mistakes.

What you’ll learn:

- Key EOFY obligations based on business structure

- How to identify and claim eligible tax deductions

- PAYG, FBT, GST, and superannuation requirements

- The importance of accurate recordkeeping and stocktakes

- Updating depreciation schedules for business assets

- Managing capital gains and losses effectively

- Benefits of engaging a professional bookkeeper

The end of the Australian financial year is fast approaching. 30 June marks the end of 2023/24 and small business owners across Australia will need to start preparing to lodge their tax returns shortly afterwards.

It can be challenging, as a small business owner, to prioritise bookkeeping when there are so many other competing priorities in your business.

However, it is a crucial aspect of running a business and compliance with Australian Tax Office (ATO) obligations is a must if you want to ensure your business is successful in the long term.

Failing to lodge your tax returns on time can incur penalties and fines, which can take up more resources to navigate, not to mention the additional stress involved.

In our latest blog, we explore the Australian end-of-financial year (EOFY) requirements for small business owners. We will also provide you with valuable tips to help you get organised in your business.

EOFY Requirements for Small Business Owners

Do EOFY obligations vary depending on your business structure?

Answer: Yes. A sole trader will have different reporting and compliance responsibilities than a company or trust. It’s essential to know what applies to your setup

Your EOFY requirements to comply with the ATO’s obligations will depend on your business structure.

A sole trader has different compliance obligations than a company or trust, for example.

The information below is designed to be a guide and a prompt for small business owners to consider when considering their EOFY requirements.

Determine Claims for Tax Deductions

What deductions can small businesses usually claim?

Answer: You can generally claim expenses that are directly related to running your business—like home office costs, travel, equipment, and software.

Deductions are amounts that you can claim for running expenses directly related to your small business. To lodge your tax return, you will need to have an idea of any claims for business-related deductions.

- Home office deductions

- Travel or motor vehicle expenses

- Machinery, equipment or tools

- Computers, IT and other infrastructure

Keep in mind that evidence will also be required to verify any deductions.

Yearly Income Tax Return Lodgement

All businesses need to lodge a tax return each year, regardless of business structure. Lodging your return on time is important to comply with ATO requirements.

The deadlines for lodgement will depend on your business structure. There are also different dates depending on whether you are lodging a business tax return yourself or engaging a tax professional to do it for you.

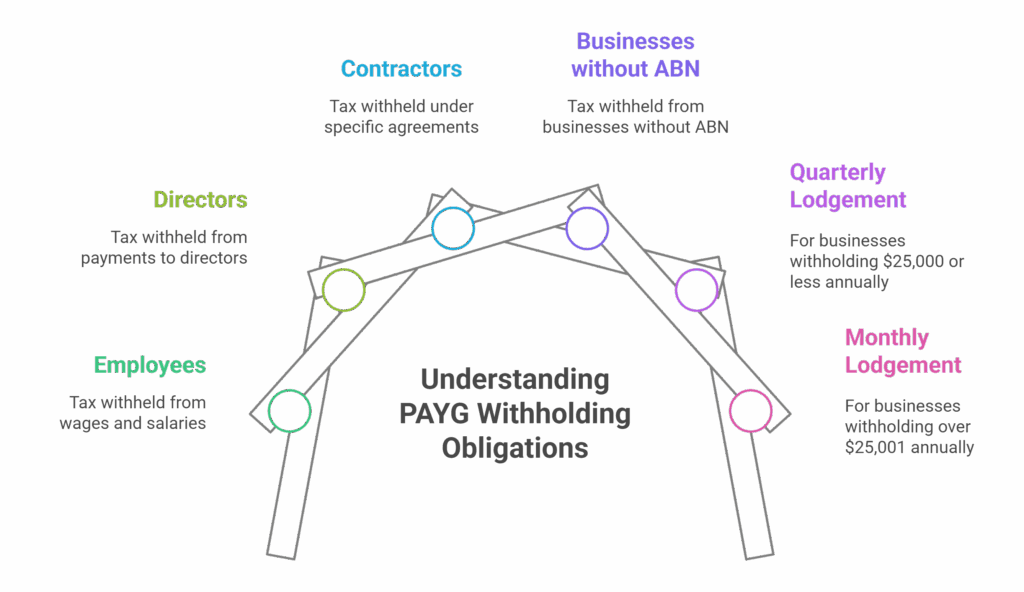

Pay As You Go (PAYG) Withholding Lodgement

What determines how often PAYG withholding must be lodged?

It depends on how much tax you withhold annually. The more you withhold, the more frequently you need to report and pay it.

Businesses need to withhold tax from:

- Employees

- Directors

- Some contractors in the case of a voluntary agreement

- Businesses that don’t tell you their ABN

Your lodgement and payment obligations depend on how much tax you withhold each year. If you withhold $25,000 or less, you can pay the withheld tax each quarter and report in your quarterly business activity statements.

If you withhold more than $25,001 to $1 million, the withheld tax will be paid each month and reported monthly.

Fringe Benefits Tax (FBT)

What are considered fringe benefits by the ATO?

Common fringe benefits include private use of work vehicles, paid entertainment, accommodation, and other perks provided to employees.

Fringe Benefits Tax is paid by employers on any additional benefits or ‘perks’ paid to an employee. This includes things such as vehicles for private use, health insurance benefits, hospitality or entertainment expenses, housing or accommodation, and other non-cash benefits. Businesses must lodge an FBT return and pay any FBT they owe.

Goods and Services Tax (GST) Lodgement

If you’re registered for GST, you will report in and pay your GST quarterly. There is nothing additional to do with GST at the end of the financial year. However, it is important to ensure that your records are up-to-date and accurate so all of your EOFY reporting will be correct.

Superannuation Obligations

Can paying super early help with tax deductions?

Yes. Making super contributions before 30 June may allow you to claim them in this year’s tax return.

If you have superannuation obligations, ensure your payments are up-to-date. You may consider making your payments early before 30 June 2024, which will allow you to claim it as a tax deduction in this year’s income tax return instead of next year.

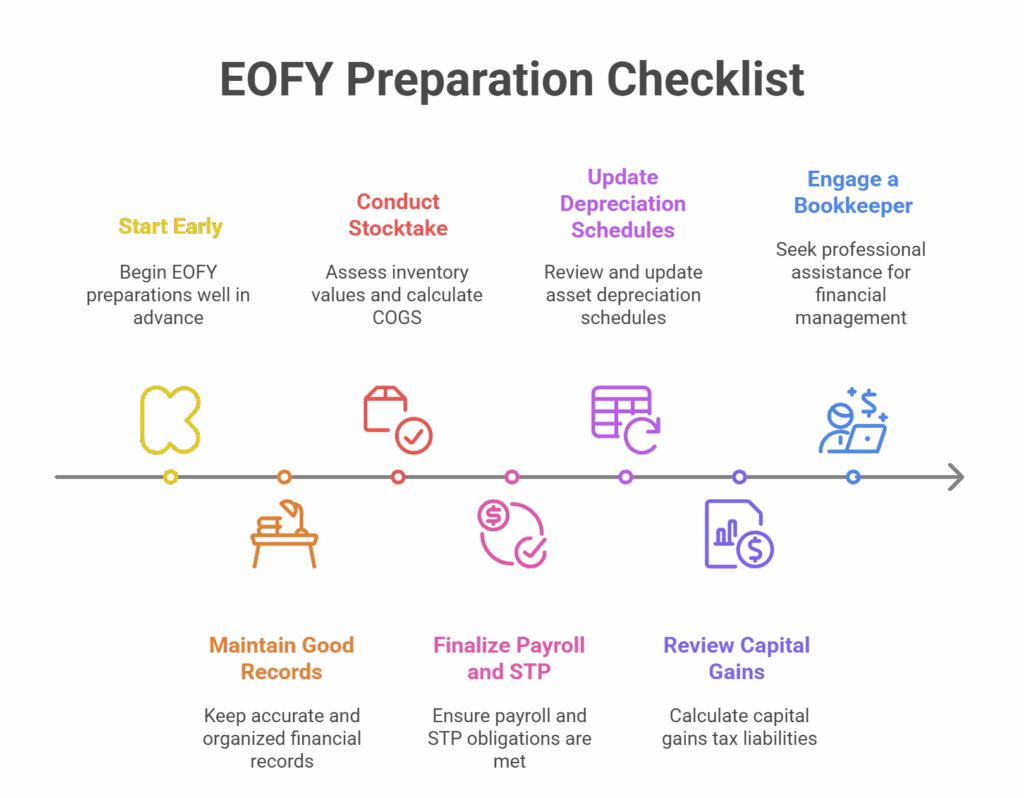

7 Tips to Get Organized in Preparation for EOFY

1. Don’t leave things until the last minute!

It’s important to start early when it comes to EOFY tax preparation. Leaving things until the last minute can result in unnecessary mistakes that can cost you in the long run.

Review your financial records now to ensure they are accurate and complete. Highlight any discrepancies and fill in any gaps.

2. Focus on good recordkeeping all year round

Keep accurate records and ensure it’s organised for easy retrieval. That includes receipts, invoices, and other finance documents.

Review your expenses to ensure you are aware of any potential tax deductions so you can maximise your tax savings.

But before you can lodge your taxes, you need to get your financial paperwork in order.

3. Do a stocktake

If you hold inventory, it’s good practice to do an EOFY stocktake. Assess inventory values and calculate the cost of goods sold (COGS) to ensure tax reporting is accurate.

4. Finalise your business payroll and STP

If you use Single Touch Payroll (STP), you won’t need to do anything additional in terms of payment summaries and annual reports.

However, you must provide payment summaries to your employees and lodge a payment summary for anything not already reported through STP.

Double-check your superannuation guarantee obligations are accurate and up-to-date to avoid penalties. Keep in mind the obligations for super are rising gradually. From 1 July 2024, compulsory employer-paid super will rise to 11.5%.

5. Ensure your depreciation schedules are updated

It’s easier to maintain depreciation schedules for all of your business assets throughout the year than trying to piece together the details at the EOFY. Leading up to the EOFY, check all asset values, consider any changes in depreciation rates, and calculate depreciation deductions so your financial statements can be as accurate as possible.

6. Review capital gains (and losses)

If you have had any capital gains or losses during the financial year, calculate your capital gains tax liabilities. By proactively managing your capital gains tax obligations, you can maximise the benefits for your business whilst also complying with your ATO obligations. It can be useful for small business owners to discuss capital gains liabilities with a tax advisor, accountant or other qualified professional to obtain advice specific to their business.

7. Consider engaging a bookkeeper

When should you contact a bookkeeper before EOFY?

Ideally, well before 30 June. A bookkeeper can organise your records, identify missed deductions, and ensure ATO compliance.

A qualified bookkeeper can help small business owners with all of these tips for EOFY preparation and more. Bookkeepers can play a vital role in helping you smoothly manage your finances, especially when things get hectic towards 30 June.

Find a bookkeeper before it’s too late!

The team at First Class Accounts can help you get ready in preparation for filing your taxes this EOFY. As a reliable partner in bookkeeping, we are trusted by many Australian small business owners to help better manage their books and maintain compliance.

First Class Accounts offers bookkeeping services, BAS, and payroll services, and we have well over 140 bookkeepers available across five states (VIC, TAS, NSW, SA, WA, and QLD). So, wherever you are, your nearest bookkeeper won’t be far away.

Contact First Class Accounts to find a bookkeeper near you before 30 June is upon you!

Frequently Asked Questions About EOFY for Australian Small Businesses

BAS & Tax Compliance for Businesses Business Growth & Strategy