This article explains why Xero bookkeeping software is a top choice for small business owners, showing how its cloud-based, intuitive platform streamlines accounting, improves cash flow visibility, ensures tax compliance, and integrates with other essential business tools. It also covers Xero’s scalability and the benefits of working with certified bookkeepers for maximum efficiency.

What you’ll learn:

- Why Xero’s intuitive design saves time for busy business owners

- How to manage all financial processes in one cloud-based system

- Real-time cash flow tracking for informed decision-making

- Easy integration with POS, CRM, and other business tools

- Features that support tax compliance and reduce admin errors

- How Xero adapts as your business grows

- Benefits of partnering with a Xero-certified bookkeeper

All the Whats, Whys and Hows of Running a Successful Independent Business

The life of a sole trader among the Australian business landscape can sometimes mirror the history of our country. It’s a story of resilience, innovation – and adventure.

It’s also hard work, with its own unique challenges.

We figure you’ve got the determination to face these challenges, but maybe you’re reading this because you have a sense that there are better ways to meet them.

And there are.

So let’s talk about how to utilise business planning to not only strike out on your own but put down your stakes.

But first, we need to get clear on everything that your life as a sole trader might entail.

What Are the Risks and Freedoms of Being a Sole Trader in Australia?

Being a sole trader comes with both freedoms and responsibilities. Unlike company structures, sole traders are personally liable for all business debts, meaning personal assets can be at risk.

But there can be business repercussions to the sole trader’s way of operating that could impact your personal life. Before we get to how to wrangle those, it can be helpful to gain a firm understanding of why that’s the case, especially when considering sole trader vs company structures.

Examples of Sole Traders in Australia

A sole trader is an individual who runs a business independently, keeping all profits but also carrying all risks. Typical examples include freelance writers, electricians, and graphic designers.

It’s a business structure that offers simplicity and direct control, where you are the decision-maker, enjoying the profits (and directly owning all risks). Understanding the difference between sole trader or company structures is crucial when setting up your business.

As a sole trader, you embody your business from a legal point of view. Unlike companies or partnerships, where the business is a separate entity, in a sole trader setup there’s no legal difference between you and your business. This structure can be helpful especially in the earliest stages of business. There’s less paperwork and more time for getting to what’s most important. The downside, though, is that risk. As a sole trader, any debts your business incurs are your personal, legal and financial responsibility. In the eyes of the state and the broader business community, the link between you and your business is direct.

Picture a graphic designer setting up shop from home, an electrician running a local business, or a freelance writer serving clients nationwide. These are all classic examples of sole traders. They have the freedom to set their own hours, choose the clients they work with, and pivot quickly as the market changes. For many, this flexibility is the main appeal—yet it’s important to stay on top of all admin tasks, as you’re the only one responsible.

How Do I Pay Myself as a Sole Trader in Australia?

As a sole trader, paying yourself is straightforward. Your business’s profit is your income. After covering your business expenses, you can simply transfer the remaining funds into your personal account. Keep clear records of these transactions for tax purposes, though. A decision to operate as (or remain) a sole trader could make sense if you prefer an uncomplicated setup, and depending on the general riskiness of your particular business, in terms of the potential legal and financial liabilities that might result from accidents or mistakes.

It’s wise to open a separate business bank account—even though it’s not legally required for sole traders in Australia. Doing so makes it much easier to track your income and expenses, keep your records clean, and avoid confusion at tax time. Consider setting aside a portion of each payment for taxes and superannuation, so you’re not caught out by an unexpected bill from the Australian Taxation Office.

Key Characteristics of a Sole Trader

- Simple setup and management: Starting is easy. Begin quickly and manage simply.

- Full control: You’re the boss. Every choice is yours to make.

- Personal responsibility: The income is all yours. So are losses and debts.

- Tax responsibility: At tax time, you and your business are one and the same. You might be able to claim extra deductions, however.

- Flexibility and freedom: Work your way. Set your own hours. Chase what opportunities you want to chase.

These characteristics highlight some of the sole trader advantages that make this business structure attractive to many entrepreneurs.

What Are the Pros and Cons of Being a Sole Trader?

Pros:

- Minimal startup costs and paperwork

- Full autonomy over business decisions

- Simpler reporting and fewer compliance obligations

- All profits go directly to you

- Ability to quickly respond to business opportunities or market changes

Cons:

- Unlimited liability—your personal assets can be at risk

- Can be harder to raise capital or secure large contracts

- Sole responsibility for legal, tax, and operational issues

- No separation between business and personal life

You should weigh these factors against your long-term goals, risk tolerance, and lifestyle preferences before deciding.

Is a Freelancer Considered a Sole Trader in Australia?

Yes, most freelancers in Australia operate as sole traders. This structure lets them offer services independently without the complexity of registering a company. Whether you’re a graphic designer, web developer, or content writer, being a sole trader allows you to control your hours, pricing, and clients.

While this offers freedom and flexibility, freelancers must still manage taxes, admin, and legal obligations themselves. It’s wise to track income and expenses from day one and consider using tools like Xero or hiring a bookkeeper to stay compliant.

If you’re moving from side hustle to full-time freelancing, start tracking your business income and expenses from day one. Consider tools like Xero, which makes sole trader accounting much easier, or partner with a bookkeeper to set up your systems right from the start.

Do Sole Traders Pay Tax in Australia?

Sole traders in Australia pay tax on their business earnings as part of their personal income. It’s essential to maintain accurate financial records and declare all business income on your personal tax return. Remember, keeping track of expenses can lead to tax deductions, potentially reducing your overall tax liability. Understanding sole trader tax obligations is crucial for compliance with the Australian Taxation Office.

You may also need to pay PAYG (pay as you go) instalments, depending on your income. Keeping detailed records of your business expenses—from office supplies to travel and marketing—will help you claim every deduction you’re entitled to. Speak with a registered BAS agent or bookkeeper for tips on tax-effective strategies and compliance.

How to Navigate Legal and Tax Obligations as a Sole Trader

There are a few details to keep in mind as an Australian sole trader, when it comes to legal and tax rules that apply to your business.

Do I Need an ABN as a Sole Trader?

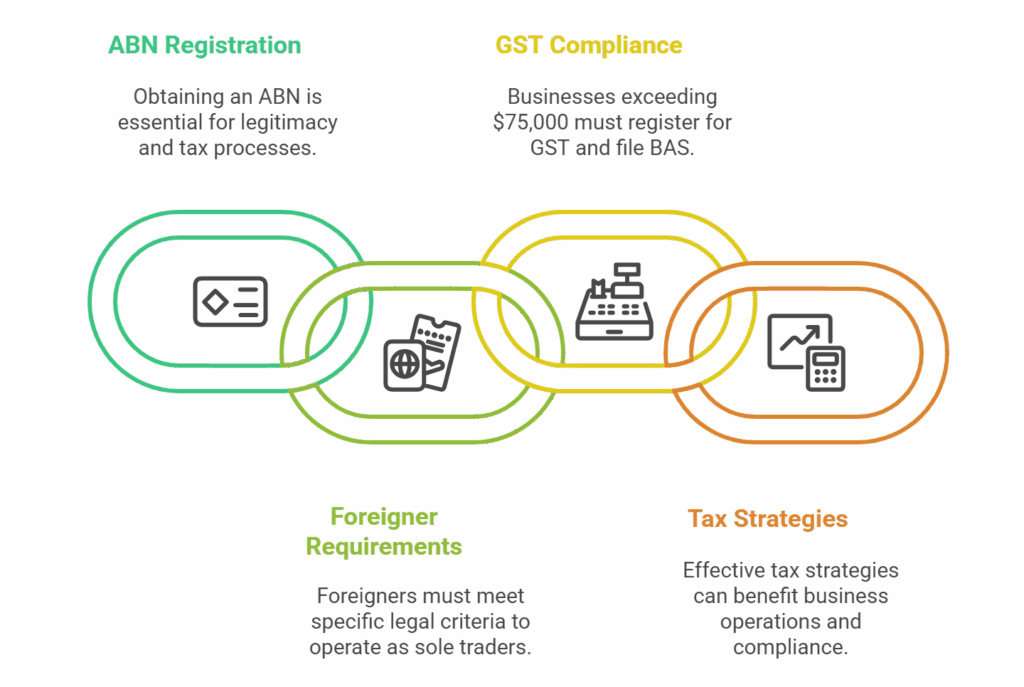

Yes. Grab your Australian Business Number (ABN) sooner than later. While your business’s income and expenses are tied to your personal taxes, an ABN helps identify your business in official matters. It’s a unique identifier that simplifies tax and other government-related processes, distinguishing you as a legitimate and operational business entity. There’s no cost to getting an ABN and the process is straightforward. The ABN sole trader registration is a crucial step in how to become a sole trader in Australia.

You’ll also need an ABN if you plan to register a business name, open a business bank account, or work with clients who require invoices. Remember, it’s a simple online process via the Australian Business Register.

Can a Foreigner Be a Sole Trader in Australia?

Foreigners can be sole traders in Australia, subject to meeting specific legal requirements. Be sure to get clear on what those may be, by consulting with an accountant and/or lawyer if exploring this possibility. Non-Australian residents will need a valid visa to obtain an ABN.

When Does a Sole Trader Need to Register for GST?

If your business earns more than $75,000 annually, you must register for Goods and Services Tax (GST). This means you’ll need to charge GST on your invoices and submit regular Business Activity Statements (BAS). While it adds some administrative work, a bookkeeper or BAS agent can help you stay compliant and claim GST credits on eligible business expenses

The main takeaway for sole traders, when it comes to taxes

Yes, you have to follow the rules. But there are also ways to make the rules work for you and your business. And they aren’t limited to optimising for tax time.

Practical Strategies for Boosting Efficiency in Your Sole Trader Business

Running a small business requires a lot of juggling. It can get hard to know where to gain back time. But here are some proven tactics to test, all of which should link up in a fairly direct way to improving your financial health as a business owner as well.

Hands-On Time Management

Effective time management buys back space for growing your business. Here are some practical tips for improving in this area:

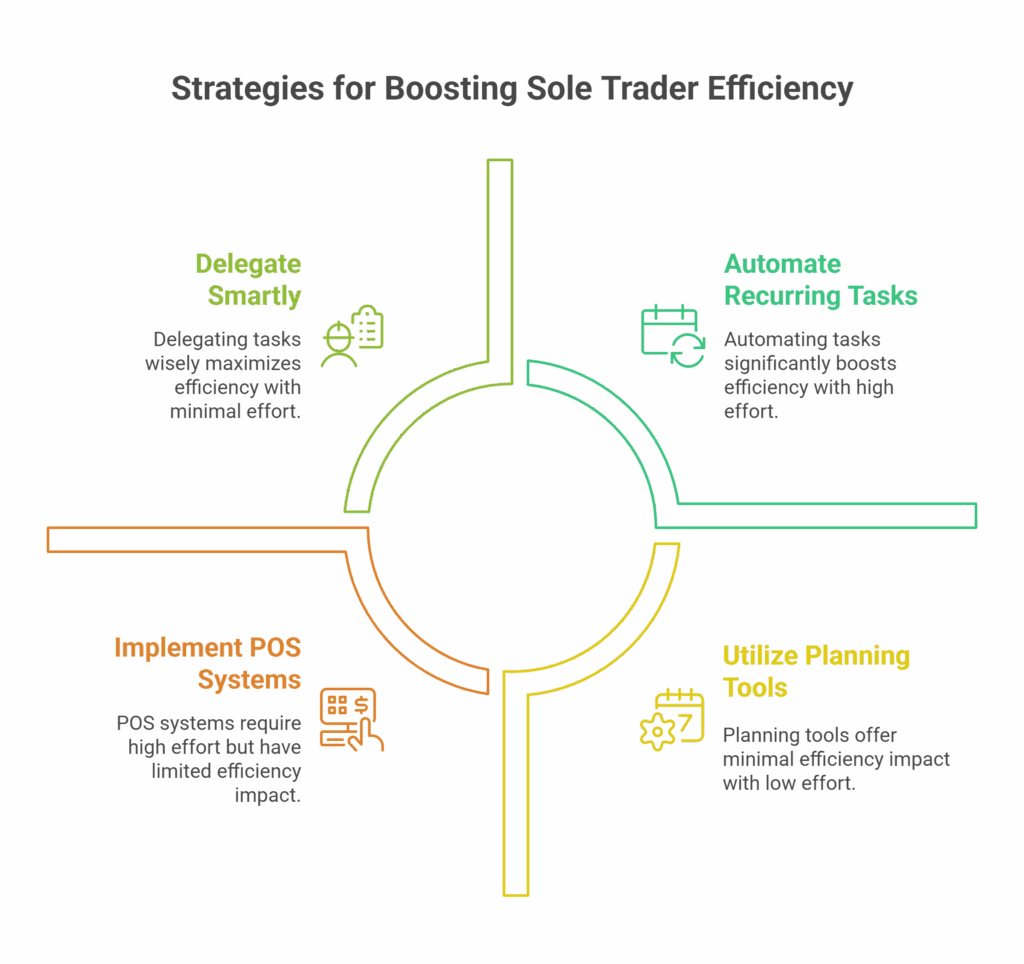

- Delegate smartly: If you employ contractors or other help, use such resources wisely. Delegate tasks based on the strengths of each contributor. This not only frees up time but empowers the people helping you.

- Efficient scheduling: Plan your days around your business’s peak hours. Schedule administrative or personal tasks during quieter periods, so you can be available when your business needs you most.

- Customer flow: If you have a store or a physical space, consider how its layout manages customer flow. A well organised and thoughtfully laid-out space can lead to more efficient service and happier customers.

Make use of simple planning tools such as calendar apps, to-do lists, or even basic project management software to prioritise tasks. The habit of reviewing your schedule at the start and end of each week can help you spot potential bottlenecks before they cause issues.

Use Tech to Simplify Things

While not every business needs the latest technology, there’s often a case to be made today for employing new solutions that save money and time, at relatively low costs.

- Point of sale (POS) systems: A good POS system can speed up transactions, manage inventory, and even offer insights into your sales patterns. Research options and select one that has features that best match your business.

- Basic accounting software: If you’re already using accounting software, make sure you’re using it to its full potential to track your finances and understand your business’s financial health. If you aren’t, consider trying out some software, or outsource your accounting to a trusted advisor. At First Class Accounts, we can help with the setup and use of all popular solutions, including Xero and Quickbooks. Proper sole trader accounting is essential for financial management and compliance.

- Social media marketing: Use social channels to connect with your community, showcase your products or services, and drive foot traffic. In today’s modernised business environment, this is arguably more of a must than a nice-to-have at this point. Effective marketing strategies can significantly boost your sole trader business.

Consider automating recurring admin tasks, like sending appointment reminders or scheduling social media posts. Many tools now offer affordable options designed for sole traders, and a little automation can free up valuable hours each week.

When to Call On Professional Support

As a sole trader, you’re at the helm of your business, balancing multiple responsibilities daily. But, especially with success, a time may come when professional support is needed to continue this balancing act.

Bookkeeping is often a good first step when it comes to bringing in outside support for your sole trader business. In addition to bringing clarity to your profit and loss statements and your tax planning, it can also provide a foundation for more insightful and effective business planning.

Professional support doesn’t have to break the bank. Even a quarterly check-in with a bookkeeper or accountant can help you spot missed deductions, ensure compliance, and put better systems in place. As your business grows, you might look to outsource payroll, BAS lodgement, or other admin tasks to further lighten the load.

Tailored Support for Real Business Needs

Effective accounting support for a sole trader doesn’t usually match up to a one-size-fits-all approach. More likely, your unique business needs will require a tailored solution.

This might look like:

- Help with day-to-day financial management

- Assistance with navigating tax requirements

- Accurate insights for making informed growth decisions

First Class Accounts: Partnering in Your Business Journey

First Class Accounts offers this kind of custom support. Our network of expert bookkeepers includes many professionals who can meet your specific needs as a sole trader, from managing your books to offering strategic business advice. A partnership with First Class Accounts can be a significant step in streamlining your operations and guiding your business toward growth. Your success as a sole trader is our success.

Steps to Set Up as a Sole Trader in Australia

- Choose your business name: Decide if you want to trade under your own name or register a business name.

- Register for an ABN: Essential for tax and invoicing purposes.

- Open a dedicated business bank account: Simplifies tracking your business finances.

- Understand your tax and GST obligations: Register for GST if you expect turnover over $75,000.

- Get insurance: Consider public liability or professional indemnity insurance to protect yourself and your assets.

- Set up basic record-keeping: Use accounting software or a spreadsheet to track income and expenses.

- Plan for superannuation: As a sole trader, you’re responsible for your own super contributions.

Taking these steps early sets you up for success and saves headaches down the track.

Understanding everything from taxes to tools will help you succeed long-term as an independent business owner.

Ready for more? If you need tailored advice or help setting up the financial side of your business, contact your local First Class Accounts bookkeeper for support that’s as independent as you are.