This article explains how small businesses in Australia are taxed, covering definitions, tax rates, and key obligations for sole traders, companies, partnerships, and trusts. It also outlines GST rules, PAYG requirements, payroll tax, and fringe benefits tax, plus practical tips to stay compliant and maximise tax concessions.

What you’ll learn:

- How “small business” is defined under Australian law

- The tax rates for sole traders vs. companies

- GST thresholds, registration, and credits

- PAYG withholding and instalment requirements

- Payroll tax and fringe benefits tax basics

- Common tax concessions for small businesses

- How a bookkeeper can help you stay organised and save money

Embarking on a business venture is thrilling, but it’s not without its complexities, especially when it comes to taxes. Whether you’re just starting or you’re already in the thick of business operations, understanding your tax obligations is vital for your success. In this article, we’re breaking down everything you need to know about small business taxes in Australia, including how much tax you will pay and how much tax a small business pays in Australia.

What is a Small Business in Australia?

A business that employs less than 20 people is considered a small business and is a tax law category of its own. According to the Australian Small Bureau of Statistics, 97% of all businesses in Australia are in this category. Understanding your business size is crucial as it affects your tax obligations and eligibility for various tax concessions.

It’s important to know your business structure as well—whether you’re operating as a sole trader, company, partnership, or trust. This not only impacts how much tax you pay, but also which tax concessions and reporting methods apply to your business.

4 Size Qualifications of Businesses in Australia

There are typically four types of business sizes:

| Category | Definition |

| Non-employing businesses | Sole proprietorships and partnerships without employees |

| Micro-businesses | Businesses employing between one and four people, including non‑employing businesses |

| Other small businesses | Businesses that employ between five and 19 employees |

| Nano businesses | Businesses that earn under $75,000 |

Depending on the size of your business, you’ll have different tax consequences and tax concessions.

As a small business, you’re eligible for several tax benefits, including lower company tax rates, simplified procedures for paying tax, and opportunities for instant asset write-offs.

What are your small business tax obligations in Australia?

Small businesses in Australia have to pay different types of taxes depending on their income, business structure, and activities. These include income tax, company tax, GST, and PAYG instalments. The business tax in Australia can be complicated and involves quarterly payments, various thresholds, and tax rates. Additionally, each Australian state, territory, and local government may implement specific tax regulations that differ from neighbouring states. Small business owners are responsible for reporting and paying various taxes, including income tax, GST, and payroll tax.

Let’s take a closer look at each of these taxes:

1. Understanding Small Business Goods and Services Tax (GST)

The Goods and Services Tax (GST) is a significant aspect of small business tax in Australia. It is a broad-based tax of 10% imposed on most goods, services, and other items sold in the country. You must include GST on your sales and remit it to the Australian Taxation Office (ATO) periodically, usually through your Business Activity Statement (BAS).

When Do You Have to Pay GST?

If your business has an annual turnover of $75,000 or more, you must register for GST and charge it on your taxable sales. This threshold is an important consideration when determining your tax obligations.

If you are under this threshold but want to claim GST credits for business expenses, you can still register voluntarily. Many small businesses choose to do so if they expect to grow quickly or want to claim GST credits on large setup costs.

2. Income Tax: Paying Your Fair Share on Business Profits

Income tax is a significant aspect of small business taxation in Australia. It refers to the tax paid on your business’s net income or profits in a financial year. As a sole trader in Australia, how much tax you pay depends on your assessable income (profit minus your allowable tax deductions on your tax return).

How Much Income Tax Do Australian Businesses Pay?

According to PWC, except for ‘small or medium business’ companies, which enjoy a reduced tax rate of 25%, all companies in Australia are liable to pay a federal tax of 30% on their taxable income. This is known as the corporate tax rate in Australia or the company tax rate.

For small businesses, the company tax rate Australia 2024 is expected to remain at 25% for base rate entities. A base rate entity is a company that has an aggregated turnover of less than $50 million and 80% or less of its assessable income is base rate entity passive income.

Sole trader tax rates for the 2023-24 financial year in Australia:

| Taxable Income Range | Tax Rate |

| Up to $18,200 | 0% (Tax-free threshold) |

| $18,201 to $45,000 | 19 cents for each $1 over $18,200 |

| $45,001 to $120,000 | $5,092 plus 32.5 cents for each $1 over $45,000 |

| $120,001 to $180,000 | $29,467 plus 37 cents for each $1 over $120,000 |

| Over $180,000 | $51,667 plus 45 cents for each $1 over $180,000 |

It’s important to note that these rates do not include the Medicare levy, which is an additional 2% for most taxpayers.

If you’re a partnership or trust, income is generally distributed to partners or beneficiaries, who then pay tax at their personal marginal rates.

3. Understanding Payroll Tax: PAYG Withholding and PAYG Instalments

Payroll tax is levied on employee wages, and the threshold varies by state and territory. As an employer, you need to be aware of two key concepts:

- Pay As You Go (PAYG) withholding: the tax businesses withhold from employee payments and report to the ATO regularly.

- Pay As You Go (PAYG) instalments: advance payments toward your expected income tax liability for the year and must be paid if your income exceeds a certain threshold.

If you have employees, you’ll need to register for PAYG withholding, regularly remit these amounts to the ATO, and provide payment summaries to your staff. If your business is growing, keeping up with these requirements can become time-consuming, which is where a professional bookkeeper can help streamline the process.

4. Fringe Benefits Tax (FBT)

Fringe Benefits Tax (FBT) is a tax paid on certain benefits provided to employees or their associates, such as cars, entertainment, or loans. If you offer fringe benefits to your employees and the total taxable value exceeds $2,000 in an FBT year, you must pay FBT. This tax is separate from income tax and is applied to the value of the benefit. Reporting and paying FBT to the Australian Taxation Office is typically done annually through your FBT return.

If you’re not sure whether your perks or staff benefits attract FBT, it’s a good idea to check with your bookkeeper or the ATO for guidance. Even some simple things—like providing work vehicles for personal use—may trigger FBT liability.

What are the Tax Differences Between Sole Traders and Companies?

As a sole trader, you report your business income and expenses on your personal tax return and pay tax at individual rates. This means that your business income is combined with your personal income, and you’re taxed accordingly.

On the other hand, companies are separate legal entities with their own tax obligations. They file a separate income tax return and pay tax at the corporate rate.

The corporate tax rate is generally higher than individual tax rates.

Another key difference is liability.

As a sole trader, you have unlimited liability, which means you are personally responsible for the debts and obligations of your business. If your business incurs debts, your personal assets may be at risk.

Companies have limited liability. This means that the company is a separate legal entity, and the owner’s personal assets are generally protected from business debts.

Additionally, there are specific tax benefits and concessions for each structure. Sole traders can access the small business income tax offset, which reduces their tax liability.

Conversely, companies can benefit from the lower company tax rate available for small businesses.

Sole Trader vs Company: A Quick Comparison

| Aspect | Sole Trader | Company |

| Tax Rate | Individual tax rates, generally lower | Corporate tax rates, generally higher |

| Liability | Unlimited liability (personal responsibility for debts) | Limited liability (owner’s assets protected) |

| Tax Benefits | Access to small business income tax offset | Benefit from lower company tax rate for small businesses |

How can small businesses stay compliant and maximise tax benefits?

Navigating the complex tax landscape is a critical component of managing a small business in Australia.

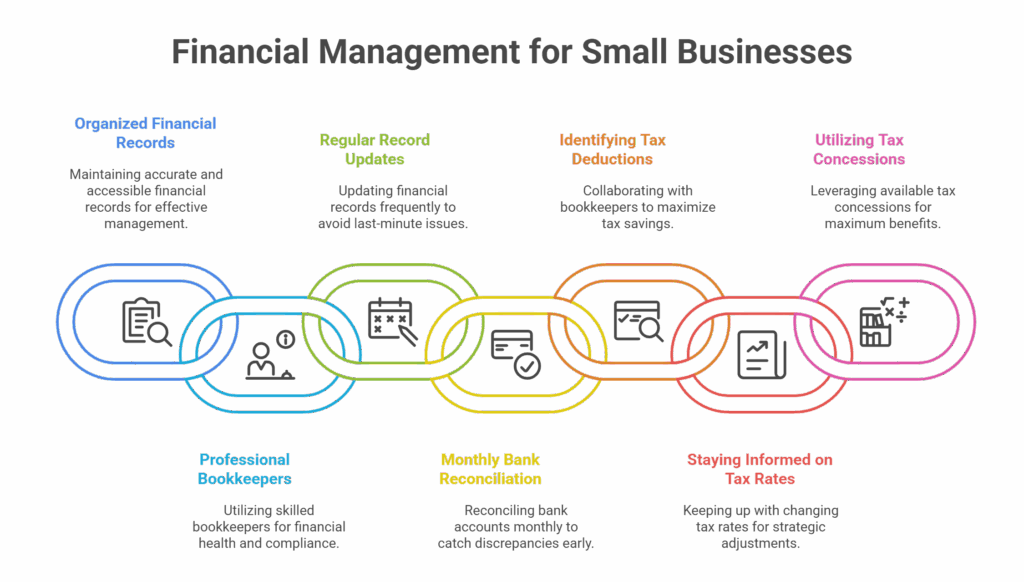

One of the most challenging aspects can often be keeping your financial records organised and compliant. This is where the role of a professional bookkeeper becomes invaluable.

A skilled bookkeeper ensures that all your business financial documents are meticulously managed, making tax time less daunting.

For many small businesses, the detailed attention provided by a bookkeeper is more than sufficient, negating the immediate need for an accountant.

Extra Tip:

Regularly updating your records and reconciling your bank accounts every month can prevent small issues from becoming big problems at year-end. Plus, by working closely with a bookkeeper, you can identify potential tax deductions, stay on top of changing tax rates, and make the most of available small business tax concessions such as instant asset write-offs or simplified depreciation rules.

How can you avoid overpaying your business taxes?

With accurate and up-to-date records, you avoid overpaying on your taxes, and you also gain clearer insights into your business finances, allowing you to make more informed decisions.

Remember, keeping accurate records is the first step to staying ahead of tax regulations and is key to your business’s success.

If you’re unsure about any part of your tax obligations or want peace of mind, consulting with a registered BAS agent or bookkeeper at First Class Accounts can be invaluable.

How a Bookkeeper Can Help You Stay on Track

A good bookkeeper will help you:

- Maintain compliance with ATO deadlines and reporting

- Keep your records audit-ready

- Identify and record all allowable deductions

- Provide regular insights into your cash flow and tax position

- Assist in preparing and lodging BAS, FBT, and PAYG documents

- Give advice on what concessions your business can access

This kind of proactive support not only saves time and stress but can also lead to real cost savings over the course of the year.

Ready to take the stress out of managing your books? Focus on what you do best – running your business. Get in touch with your local First Class Accounts bookkeeper for a free consultation and see how we can help simplify your small business tax.